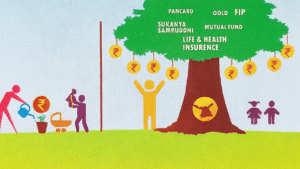

Let’s educate the child Financial Planning for Children and Retirement.

It is not right to think that the real responsibility is to give full love to the children born in the womb. If they want to have a good life, you have to be a little stubborn in financial matters! Whether you want to educate your children in a higher way, or to educate them heavily for their marriages… While they are still young, make a wish with a saving mantra and make an amulet with an investment machine.

Start investing in their name on the day of naming the child. There are various ways available for this. Whether you do SIP or choose Sukanya Samriddhi Yojana, the interests of the child should be paramount. Choose schemes that will be the backbone for higher education, marriage, and settlement matters and share your responsibilities happily.

As soon as you receive the birth certificate, you should get Aadhaar. It is also advisable to get a PAN card first. Having a PAN card is very important for bank transactions and other investment management later. If you send the Form 49A application along with the child’s Aadhaar, personal certificates of the parents, and address proof documents to the National Securities Depository Limited (NSEL)-Pune center, you can get a PAN card.

Starting with a bank account

For investments to run smoothly, it is better to have them in the name of the child. It is not enough to think that you are saving by depositing them in the parents’ savings account. When something needs to be done, the thought of using the money in the account comes first. If you deposit it in the child’s name, your mind will not turn to them unless it is urgent. Opening an account for minors is now very easy. A birth certificate and Aadhaar card are enough. You will have to add the PAN and phone number of the parents, but if you have the same bank as your account, then that is not necessary. A minimum balance of Rs. 2,500 to Rs. 10,000 has to be maintained in the minor’s bank account.

Mutual Funds and sip

After getting a bank account.. it is very easy to maintain a mutual funds account in their name, start an SIP with a small amount depending on your financial situation. A birth certificate is enough to open a mutual funds account. A canceled check related to the parents’ account needs to be attached. If the children are a little older, you can give a canceled check related to their account. If you are thinking about mutual funds.. if it is a girl child, you can invest in the Sukanya Samriddhi Yojana scheme. If you invest so many thousands per month in that scheme.. the profits will increase as the children grow up. The small amount you save every month will help them a lot.

Invest in gold

There is no better way to invest than gold. Even if your daughter can buy a pound of gold for every birthday.. by the time the baby turns five, gold will accumulate in the pocket. This will prevent you from having to pay the burden of gold for your daughter’s wedding. If you need funds during your higher studies… it will be easy to take a loan against gold. If you find it difficult to store gold at home… digital gold investment is better.

Health protection

‘Elders say to rise above the bad. No matter how many investments you make in the name of your children… if the health condition of your parents deteriorates… you may not be able to continue those investments. If you don’t want such a day to come… you must have a protective shield for your health! Before investing in the name of your children, get health insurance in your family’s name and life insurance in your name.

Sukanya Samriddhi Yojana

2. 5,000

Returns: 8.2 percent (annual)

* Total return over 18 years: Approx. Rs. 23.81 lakh

SIP

” Monthly: Rs. 5,000 (Nifty 50 Index)

# Returns: 12.44 percent (approx.)

” Total return over 18 years: Approx. Rs. 37.29 lakh

Why is the climax difficult?

‘How many years have you been wearing clean clothes? How many years have you been eating two meals a day?..’ These are the words of Allu’s character Shankara Sastri in the movie Shankara Bharanam, while confronting him! In the movie, Shankara Sastri is said to be passionate about music. But, in real life, there are many gentlemen who have the opportunity to spend the rest of their lives in a special way… but they are seen to be content.

Even though they have assets worth lakhs of rupees… they live without a single penny in their hands. They pass on everything they have accumulated to their heirs, leaving them anonymous! If you don’t want to face such difficulties, don’t submit to such conditions…

A recent article was published saying, ‘Senior citizens in India are living in poverty… and are becoming rich. What is the point of becoming rich after a person who is in poverty dies?’ You may wonder. Some people consider accumulating assets as their first duty… and consider it a serious crime to enjoy them for their own. They continue to follow the strict rules followed in the process of accumulating those assets. Since all their income is in the form of properties… they do not have enough money for daily expenses. Due to this, even if they have eight lakhs in their property documents..

They face worries about the currency. Moreover, they are emotionally connected to those assets. Even if emergency situations arise, they do not dare to sell a cent of land to make money. Will their heirs properly respect those who have acquired inexhaustible assets for generations? In the case of some, that becomes greed. As shown in movies.. They act as if ‘if this man goes, we will not get the property’!

Property-income..

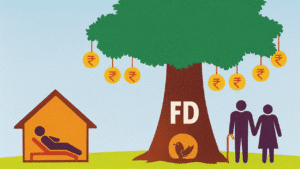

We should first know what real property is! Real wealth is what is done without suffering. Real property is what is supported in times of loss. When both of these are useless, what is the benefit? There is no way to live according to property. It depends on income. When you buy property, there should be some income from it. No matter how many properties do not create wealth, it is useless! A man bought a thousand-yard plot at the end of the village with the money he had saved throughout his life!He decided to give it to his two children and his son in equal shares after his death. So far, so good. In these days, when we give the utmost value to the unfortunate, this man is not in a position to take care of the property that will come to him someday. Moreover, demands are being made to give equal shares to all three of us in the land that will come to him someday. If this same man buys a field with some of that money, he will reap the harvest. In the form of a house, he will get a monthly income in the form of rent until he passes away. If he deposits the remaining half in the bank, he will get interest. There is no need to live on anyone’s kindness.

Give relief. Financial Planning for Children and Retirement

If a movie wants to be a hit… no matter how the first half is, the second half should be perfect. If there are difficulties in the climax too… the audience will be speechless. The end of life should also go smoothly. To avoid dependence on anyone, you should ensure that you get a regular income every month. You should ensure that your lifestyle is not disrupted. You should keep your emotions under control in old age. When the retirement money comes, you call your sons-daughters, daughters-in-law and give them everything… if you think that the responsibility is over… you are wrong. Retirement life should be a relief for the hardships you have faced all these years. To do that… your property should be in your hands.

That Instead of being useless assets, you should ensure that they are in the form of income-generating, liquid assets. Suppose you have one crore rupees. If you do FA in the bank, you will get Rs. 60 thousand per month. With that, you can live comfortably. After you, that crore rupees will go to your nominees! Remember that if you distribute that crore rupees in advance, your life story will end in tragedy.

✨ About Me

Hi! I’m Manikanta Reddy, a passionate finance enthusiast with a strong understanding of money management, personal finance, and smart investment strategies. I believe financial literacy is the foundation of a secure and stress-free life — and I’m here to share practical insights, real-life examples, and simplified advice to help you make better financial decisions.

Whether it’s choosing between paying off a loan or investing, building emergency funds, or planning for retirement — I love breaking down complex topics into easy, actionable tips that anyone can follow.

Let’s learn, grow, and build wealth — the smart way. 💰