Buy a House… Not Tension!

“Think Before You Buy: A Reality Check for First-Time Homebuyers”

For many, the dream of owning a house is slowly turning into a reality. With young professionals landing prestigious jobs at an early age, thoughts of homeownership arise quite early—sometimes even before marriage. However, it is crucial to ask yourself two questions before taking the plunge:

When should you buy a house?

Why are you buying it?

You should only move forward if you’re clear and confident about both.

A Generation Chasing the Ideal

“House.. House.. Children”—this was the title of a movie that came out decades ago. Interestingly, today’s generation seems to have taken that title quite seriously. The moment they land a job, many dream of settling down with a spouse in their own house.”Think Before You Buy: A Reality Check for First-Time Homebuyers”

These hopes and aspirations, though well-meaning, often lead to overexcitement. Even without a rupee in hand, people go hunting for their dream home, relying heavily on bankers and home loans. As soon as they find a place they like, they pay a token amount to the builder and pin their hopes on a quick loan sanction.

True, a decent salary can easily fetch a big loan, but many forget the most important part—EMIs are forever.

How Much Do You Really Have?

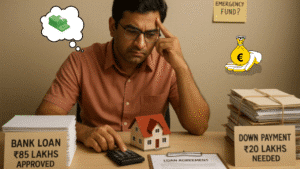

Income alone is not enough to buy a house. Financial preparation is key. Let’s say you earn Rs. 1.5 lakh per month. Buying a Rs. 1 crore house may not seem like a big issue. But here’s the breakdown:

-

Home loan = Rs. 85 lakhs

-

Your contribution = Rs. 15 lakhs

-

Registration, stamp duty, and fees = Rs. 3 lakhs

-

Housewarming, furnishing, moving expenses = Rs. 1–2 lakhs

That’s a total upfront cost of Rs. 20 lakhs or more.

Now, banks will happily approve that Rs. 85 lakh loan in hours. But where will the remaining Rs. 20 lakhs come from?

If you’ve saved it—great. If you’re borrowing it from elsewhere (personal loan, gold loan, friends/family), you’re just stacking one loan on top of another. That’s a recipe for financial stress.

“Think Before You Buy: A Reality Check for First-Time Homebuyers”

Pro Tip:

Always have a 6-month emergency fund set aside even after making your down payment. Life is unpredictable—job loss, illness, or emergencies can hit anytime. A home should not leave you helpless.

If You Are in Debt…

Any investment should bring peace of mind, not take away the happiness you already have.

Many make the mistake of thinking, “Once I get the house, everything else will sort itself out.” In reality, it doesn’t work like that.

-

EMIs will keep coming month after month.

-

Property taxes, maintenance charges, society fees, and occasional repairs will follow.

-

And if you already have other loans (like for a car, personal expenses, or business), your monthly commitments could become unbearable.

It’s better to wait and save than rush into a house that ties you down. “Think Before You Buy: A Reality Check for First-Time Homebuyers”

Example:

Someone earning Rs. 80,000 per month might manage a 35,000 EMI—but what if they have Rs. 15,000 going toward personal loans and Rs. 5,000 toward insurance premiums? Add daily expenses, and there’s barely anything left.

Don’t Go Overboard

If you’re thinking about buying a house, don’t be discouraged by these warnings. This isn’t negativity—it’s realism, so you can actually enjoy your home once you move in.(“Think Before You Buy: A Reality Check for First-Time Homebuyers”)

If you look at your home only as an investment, you might hesitate too long. But if it brings joy and security, and it’s within your financial means—go ahead. Just make sure:

-

You aren’t buying a house just because others are.

-

You’re not holding back from buying just because someone else told you not to.

-

You are not blindly trusting real estate marketing—do your own research.

Things to Check Before Buying a House (“Think Before You Buy: A Reality Check for First-Time Homebuyers”)

Here’s a quick checklist before making the leap:

✅ Down Payment Ready (At least 15–20% of property value)

✅ Emergency Fund Maintained (6 months of living expenses)

✅ Low or No Existing Debt

✅ Fixed Job with Steady Income

✅ Future Commitments Calculated (kids’ education, parental care)

✅ Thorough Property Verification (legal, location, resale potential)

✅ Comfortable EMI Ratio (EMI should not exceed 35–40% of your net monthly income)

Final Word

Consider your family’s needs—elderly parents, children’s education, your lifestyle, your future goals. Calculate how much money you can actually allocate without strain. Only then should you make your dream a reality—and yes, only after you’ve prepared your down payment!

Buy a house—not tension.

TAGS :

home buying tips, first-time home buyer, real estate advice, buying a house in India, EMI planning, home loan tips, financial planning, smart home buying, house buying checklist, emergency fund, property investment, budgeting for a house, avoid home loan stress, debt management, home buying mistakes, financial literacy, real estate planning, young professionals and housing, house vs peace of mind, personal finance for millennials

✨ About Me

Hi! I’m Manikanta Reddy, a passionate finance enthusiast with a strong understanding of money management, personal finance, and smart investment strategies. I believe financial literacy is the foundation of a secure and stress-free life — and I’m here to share practical insights, real-life examples, and simplified advice to help you make better financial decisions.

Whether it’s choosing between paying off a loan or investing, building emergency funds, or planning for retirement — I love breaking down complex topics into easy, actionable tips that anyone can follow.

Let’s learn, grow, and build wealth — the smart way. 💰

Good information 👍 keep it up